Why “Qualified” no longer means “comfortable” for many Capital Region buyers

A HUDPRO Research Report

A note before you read this

I sold HUD homes in the Capital Region for twenty years. I helped close to two hundred families buy a house that the federal government had foreclosed on, fixed almost nothing, and put back on the market at a price working people could afford. Most of those families would not be able to buy those same houses today, in those same neighborhoods, at the prices those houses now command.

This is the second of two studies HUDPRO has published this month on the same problem. The first one — A Quiet Pipeline — looked at what happens to foreclosed FHA homes that used to anchor working-family homeownership. Most of them, it turns out, no longer reach the public HUD market.

This one looks at what happens to households trying to buy a regular, non-distressed home in the Albany–Schenectady–Troy market. The two studies tell one story from two ends.

— Mike Belanger, Founder, HUDPRO

The housing reality in 2026

For many Capital Region households, the housing challenge in 2026 is no longer simply whether they can qualify for a mortgage. It is whether the payment still looks workable once taxes, insurance, escrow, and upkeep are all in view.

HUDPRO analyzed current market conditions across the Albany–Schenectady–Troy market using median sold home pricing, mortgage rates, taxes, insurance, PMI, and affordability guidance to chart the widening mismatch between loan eligibility under modern FHA and low-down-payment qualification standards and what many households judge they can carry comfortably using typical conventional mortgage guardrails.

The findings echo what many local buyers describe in interviews and tours:

“We qualify, but the payment scares us.”

That pattern — cleared to borrow, uneasy about the obligation — is the qualification-to-comfort tension this study examines.

Based on current market conditions and traditional affordability guidance:

HUDPRO uses median sold pricing — not active listing pricing — as the primary affordability benchmark. Sold pricing reflects actual successful transactions. Active listing pricing is referenced separately as an inventory-pressure indicator.

To put this in real terms, consider one Capital Region couple I worked with recently. Names changed; details are real.

Kathy and Jeff are in their fifties. She works in an office in downtown Albany. He’s a welder. Combined income around $110,000. They have a house they bought in their twenties on a road that used to be quiet and isn’t anymore. They want to move — somewhere rural in Albany County, at least an acre, twenty to thirty minutes from her work. Not extravagant. They were pre-approved for an FHA mortgage up to $300,000 and decided on their own that they would not go above $280,000.

They have been looking for months.

What they have found is that the houses in their price range either sell within days to cash buyers, or have wet basements, foundation issues, or septic problems they cannot afford to fix on top of the down payment. On the few lots that worked, the well and septic setback rules left no buildable room for the workshop Jeff needs.

Housing professional with 23 years of experience in HUD-focused real estate and HUD-regulated housing workflows. About the author →

This article is HUDPRO editorial analysis. For external headlines, open Market News. By List is the live HUD inventory stats view; the map is where listings live.

There are many Kathy-and-Jeff households across the Capital District right now. The specifics vary — different towns, different jobs, different price ceilings — but the pattern is the same. Cleared to borrow. Uneasy about the obligation. Looking at listings that skew toward problems or luxury. Walking away from the math.

If you grew up in this region, you already know most of what follows. If you didn’t — if you moved here for work, if you’re under forty, if your parents bought a house somewhere else — there’s a piece of history you may not have, and the rest of this study is harder to make sense of without it.

The neighborhoods Kathy and Jeff drive past every day were not built by the market deciding, on its own, to construct affordable houses for working people. They were built by the federal government deciding, deliberately and at scale, that millions of working-class families should own homes — and writing the checks to make that happen. Between 1934 and 1962, the federal government subsidized roughly $120 billion in new housing in then-current dollars, roughly $1.2 trillion in today’s money. The Federal Housing Administration insured the mortgages. The GI Bill backstopped the down payments. The Housing Act of 1948 made FHA financing broadly available. The combined effect was a federal sledgehammer of subsidy and light regulation that let private “merchant builders” mass-produce single-family homes for under $10,000, with floor plans simple enough to put up a hundred Capes in eighteen months.

In the Capital Region, that sledgehammer landed in specific places you can still drive through today. In Albany, it built Crestwood, the postwar development behind St. Peter’s Hospital — rows of brick and wood-sided Capes and ranches put up in the late 1940s and 1950s for returning veterans and the working families who staffed the hospital, the state offices, and the new suburban commute downtown. In Rotterdam, it built Cold Brook on the former Campbell estate — one of the region’s most textbook examples of a mass-produced postwar neighborhood, designed for the General Electric workers who needed somewhere to live within reach of the plant. Adjacent Colonial Manor added more starter homes for GE employees through the 1950s. In Troy, it built Sycaway and the East Side / Albia expansion up the hill from Hoosick Street — smaller-scale developments than Rotterdam’s, but built with the same federal incentives, for the workers who powered Troy’s still-active industrial sector. These are not unusual neighborhoods in the Capital Region. They are the standard postwar housing stock of the entire metro. They are where the Capital Region’s middle class was built.

One honest qualifier the country still owes itself: the FHA program that built those neighborhoods was racially restricted by design. FHA underwriting redlined Black neighborhoods. Many postwar developments excluded non-white buyers through deed restrictions or financing barriers. Only about 2% of that $120 billion in federal housing subsidy reached non-white households. The country has spent every decade since trying to undo the damage of that exclusion, and is still trying. But the structural lesson sits alongside that one and matters here: working-family homeownership in the Capital Region was federal policy. It was not a market outcome.

That apparatus still exists. The FHA still exists. The 203(k) renovation loan still exists. The HUD Homes program still exists. None of it was abolished. It has, over decades, been redirected. The fixable, distressed houses in Crestwood and Cold Brook and Sycaway — the inventory that used to enter the public HUD market and get bought by the next generation of working families — are now being routed to investor auctions before working buyers ever see them. The neighborhoods the federal sledgehammer built are now exactly the inventory the federal pipeline is quietly diverting elsewhere.

That is the system Kathy and Jeff are searching in.

Households searching for homes in the Capital Region are not necessarily failing to qualify for mortgages.

Instead, they are reaching a different conclusion: the monthly payment no longer feels financially safe.

Common themes from local buyers include:

The challenge is balancing ownership costs against childcare, transportation, groceries, student loans, utilities, repairs, rising insurance costs, and the uncertainty of future expenses.

That widens the distance between what lenders may approve on paper and what households judge they can carry while still reserving margin for savings, maintenance, and routine shocks.

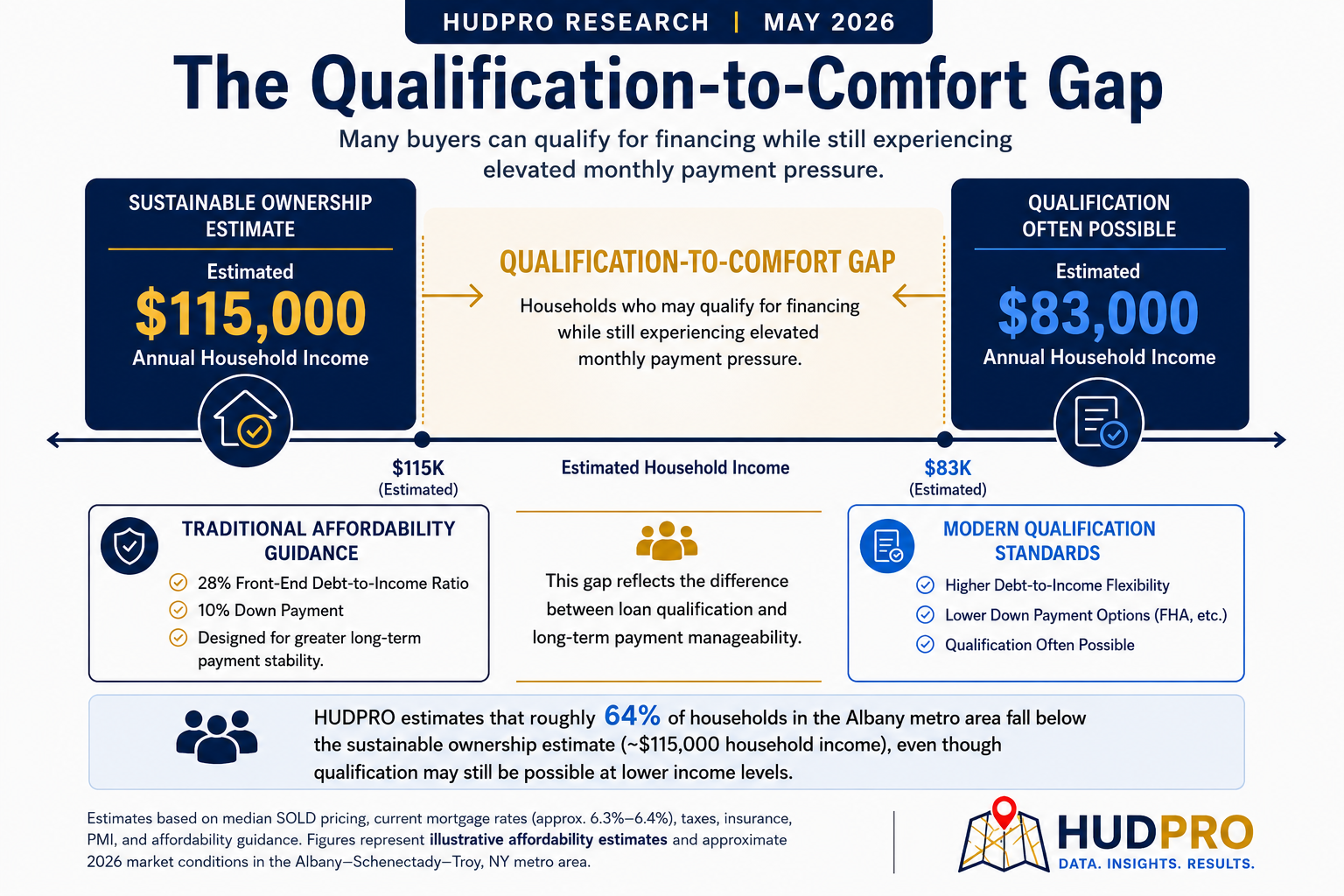

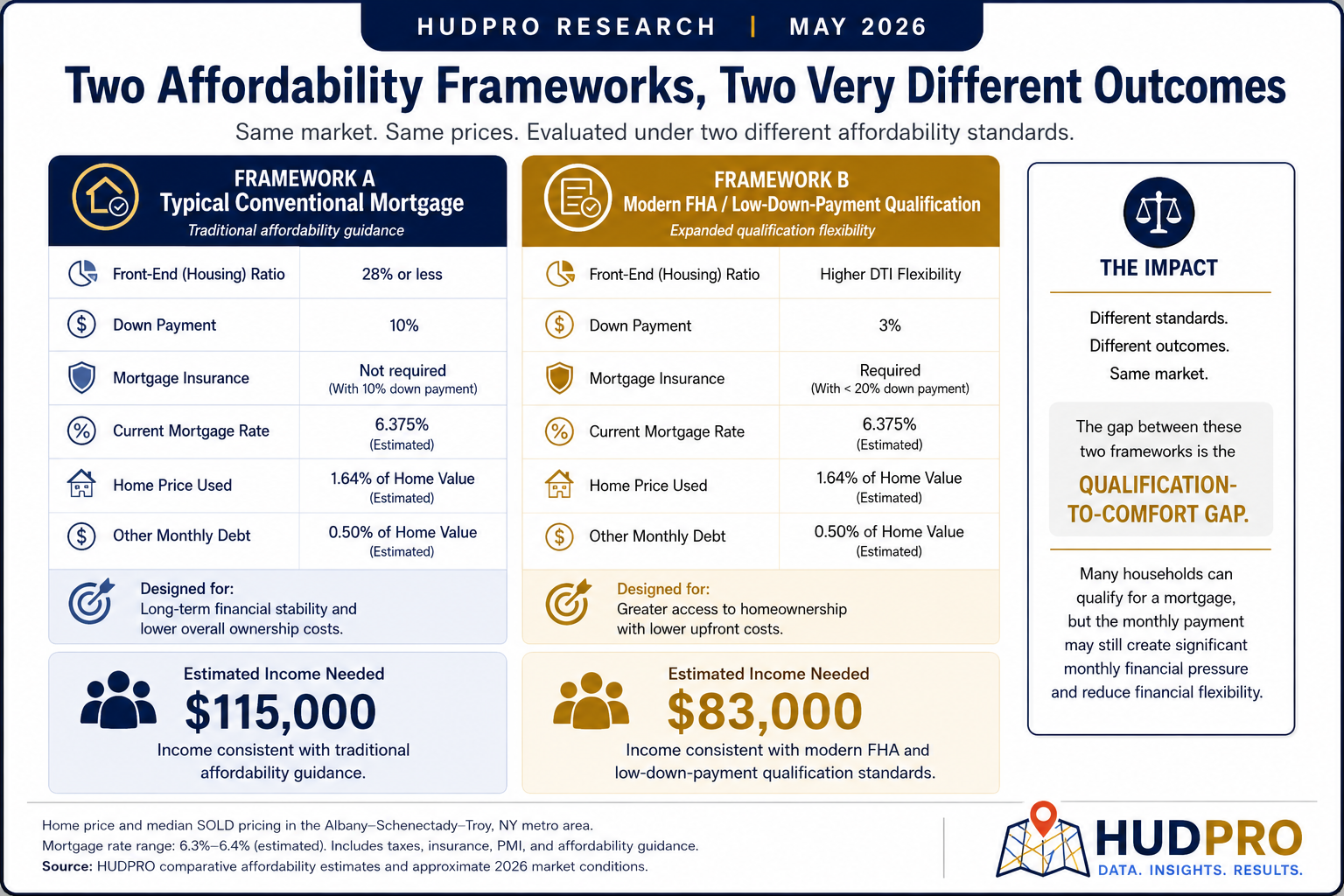

HUDPRO’s analysis identifies two different affordability realities currently shaping the Capital Region housing market.

This model reflects typical conventional mortgage standards — affordability guidance oriented toward long-horizon viability.

Assumptions include:

Under this framework:

This does not mean those households cannot buy homes. It means many may experience significant affordability pressure once the full monthly ownership burden is considered.

Compared with typical conventional mortgage guardrails, many buyers today can qualify through low-down-payment qualification programs — options households often choose to reduce upfront cash requirements.

This framework reflects FHA-style qualification flexibility, lower down payment programs, and additional debt-to-income flexibility versus many conventional mortgage benchmarks.

Under this framework:

In other words, a large share of households may still qualify for financing while simultaneously feeling financially stretched by the long-term monthly obligation.

That distance between approval using low-down-payment qualification flexibility and comfort under typical conventional mortgage guardrails is what this dual-threshold comparison isolates.

The affordability issue facing buyers in 2026 is not always whether they can obtain a loan.

Increasingly, it is whether ownership still feels compatible with emergency savings, retirement planning, childcare, future repairs, rising taxes and insurance, or the flexibility to absorb financial shocks.

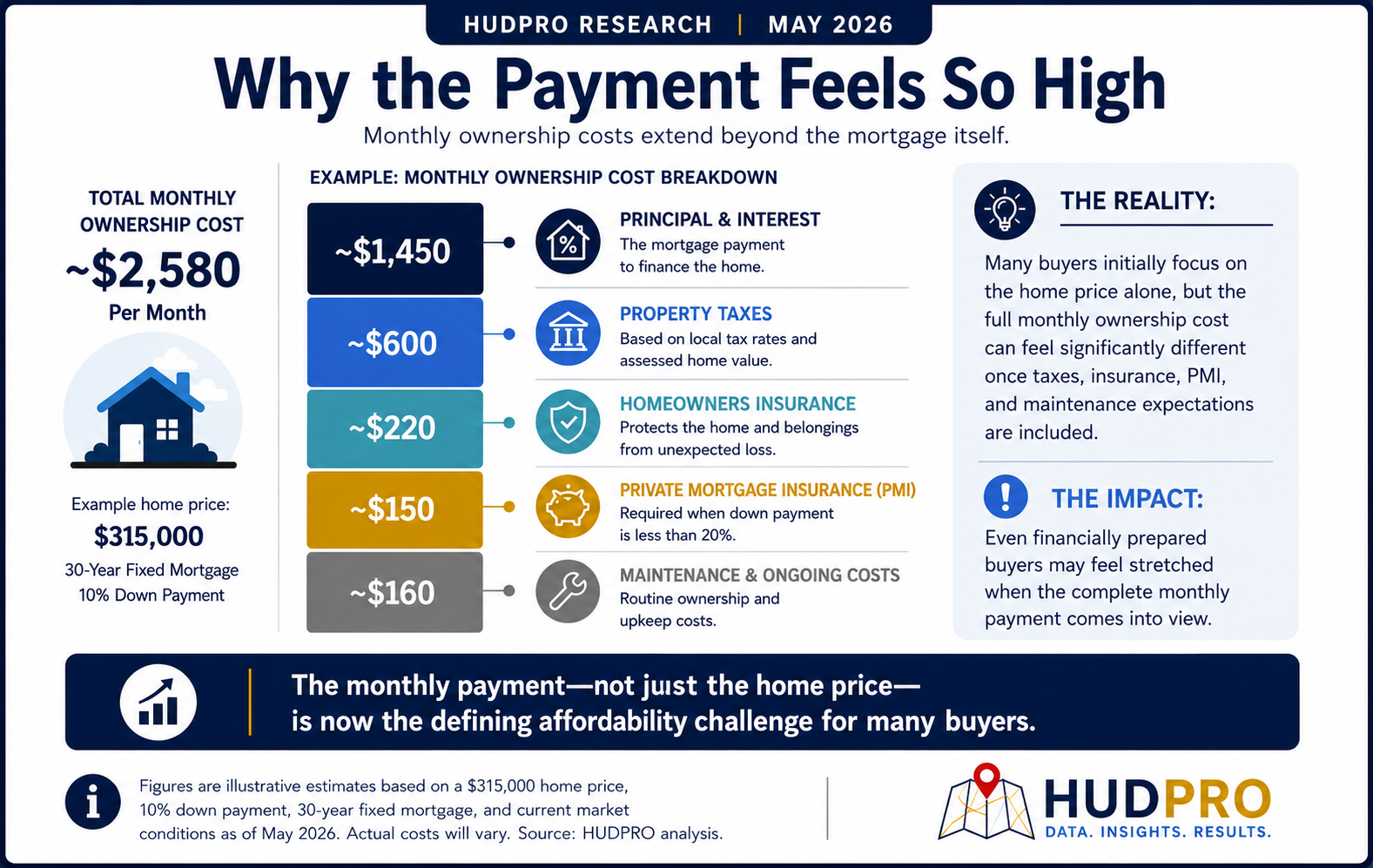

Take a household earning about $85,000: it may still clear lender underwriting when taxes, insurance, and PMI are modeled loosely or deferred to escrow estimates that firm up late in the process. Add a realistic maintenance reserve, and modest flexibility for tax or premium increases, and the residual monthly cushion often narrows sharply — even when the deal still looks approvable on the front end.

The issue is no longer simply qualification. It is confidence.

For many, the turning point comes after reviewing the actual loan estimate and ownership breakdown.

What initially appears manageable at the listing price often changes once buyers see property taxes, insurance, PMI, escrow requirements, cash-to-close estimates, maintenance expectations, and utility costs.

That is frequently the moment when buyers pause their search, lower their budget expectations, delay purchasing, or return to renting temporarily.

The issue is often not qualification alone — it is whether the finalized payment, once every line item is fixed, still aligns with how buyers budget the rest of their month.

While median sold pricing in the Capital Region remains significantly below some active listing-price averages, buyers still describe the market as financially intimidating and psychologically exhausting.

One reason is that active inventory and sold-market data increasingly reflect two different realities.

Lower-priced and move-in-ready homes often sell quickly, sometimes within days. Higher-priced homes and luxury inventory typically remain active longer, giving active listing data a disproportionately high-end skew.

As a result, the homes buyers continue seeing online are often significantly more expensive than the homes that are actually closing.

HUDPRO estimates that while median sold pricing in the Albany–Schenectady–Troy market likely falls within the mid-$300,000 range, the median active listing price during the same period was substantially higher — reflecting inventory pressure, limited supply, and higher-end listings remaining on the market longer.

That gap has become another psychological pressure point for buyers attempting to navigate the current market.

Lower-priced homes still exist in parts of the Capital Region. However, many require significant updating, deferred maintenance work, renovation financing, or a higher tolerance for repairs than many first-time buyers are financially prepared for. A lower purchase price does not always translate into lower long-term ownership risk.

There is one more piece of this market most buyers do not know about.

Across the country, HUD’s portfolio of foreclosed FHA homes available for public purchase has shrunk by approximately 74.6% since January 2022 — from 22,785 properties down to 5,803 as of April 2026. That decline is not because foreclosures stopped happening. It is because HUD has spent the last three years tuning a program called CWCOT — Claims Without Conveyance of Title — that routes most foreclosed FHA homes directly to investor auctions before they ever reach the public HUD market.

Across 2023, 2024, and 2025, roughly two out of every three FHA foreclosure dispositions sold through third-party channels rather than reaching the public HUD inventory. In the first quarter of 2026, the ratio widened to roughly three-and-a-half to one.

The foreclosed houses that used to become HUD homes — the lower-priced, fixable starter inventory in Capital Region neighborhoods like Crestwood in Albany, Cold Brook in Rotterdam, and Sycaway in Troy — are now being sold to institutional buyers before working families ever see them. These are the original FHA-built postwar middle-class neighborhoods, the inventory that used to be attainable before the pipeline started filtering it through investor auctions. Many are now being renovated and resold months or years later at prevailing market prices that include the investor’s profit margin.

The full mechanism is documented in HUDPRO’s companion study, A Quiet Pipeline. The relevance here is straightforward: the inventory channel that used to absorb working-family demand for entry-level homes has been narrowed by federal policy choices over the past decade. Households like Kathy and Jeff’s are now competing for the remaining non-distressed inventory in a market whose listed prices skew toward problems and luxury.

Some buyers across the region continue to delay purchasing decisions while hoping mortgage rates decline, inventory improves, or pricing pressure softens.

Lower rates would likely improve affordability. However, rates alone may not fully resolve the broader affordability pressures shaping today’s market.

Taxes, insurance costs, inventory shortages, and higher monthly ownership expenses continue to play an increasingly important role in overall housing affordability.

The modern housing challenge is not driven by one variable alone. It is the combined weight of home prices, borrowing costs, taxes, insurance, maintenance, and how thin those layers leave the monthly margin.

Some buyers assume HUD homes are severely distressed, investor-only opportunities, or unlivable without major reconstruction.

In practice, condition and pricing span a wide band. Some properties require substantial rehabilitation. Others need only cosmetic updates. Some represent among the few remaining ownership entry points below prevailing retail market pricing — particularly for buyers willing to accept cosmetic work or delayed updates.

However, lower pricing alone does not automatically solve the broader affordability pressures facing households. Even discounted homes must still be evaluated against taxes, insurance, repairs, whether the payment fits after realistic reserves, and long-term flexibility if income or costs shift.

The findings in this study align with broader regional and national housing affordability research showing growing pressure on middle-income households attempting to enter today’s market.

The emphasis is shifting from approval alone toward whether the fully loaded monthly obligation — principal, escrow, insurance, and a modest repair allowance — still preserves slack for non-housing essentials and savings.

In today’s market: qualified and comfortable are no longer the same thing.

There are Kathy-and-Jeff households in every Capital District town right now, watching listings, doing the math at their kitchen tables, walking away from approvals they could legally take. The federal sledgehammer that built Crestwood, Cold Brook, and Sycaway — and every neighborhood like them across the country — still exists in name. It has not been abolished. It has been redirected. Working families in markets like ours are living with the consequences of that redirection without ever having had a national conversation about whether they wanted to be redirected.

HUDPRO used a dual-threshold affordability framework to evaluate current housing pressure in the Albany–Schenectady–Troy market.

Sustainable Ownership Model assumptions:

Example ownership estimate using a median sold home price in the mid-$300,000 range:

Modern FHA / Low-Down-Payment Qualification Standards:

HUDPRO also modeled modern FHA and low-down-payment qualification standards — programs buyers often use when seeking lower down payments or higher allowable debt-to-income flexibility than many conventional benchmarks emphasize.

This framework reflects loan eligibility many buyers may reach — even when the resulting payment still feels demanding month to month.

Qualification examples are simplified illustrative scenarios and not lending advice.

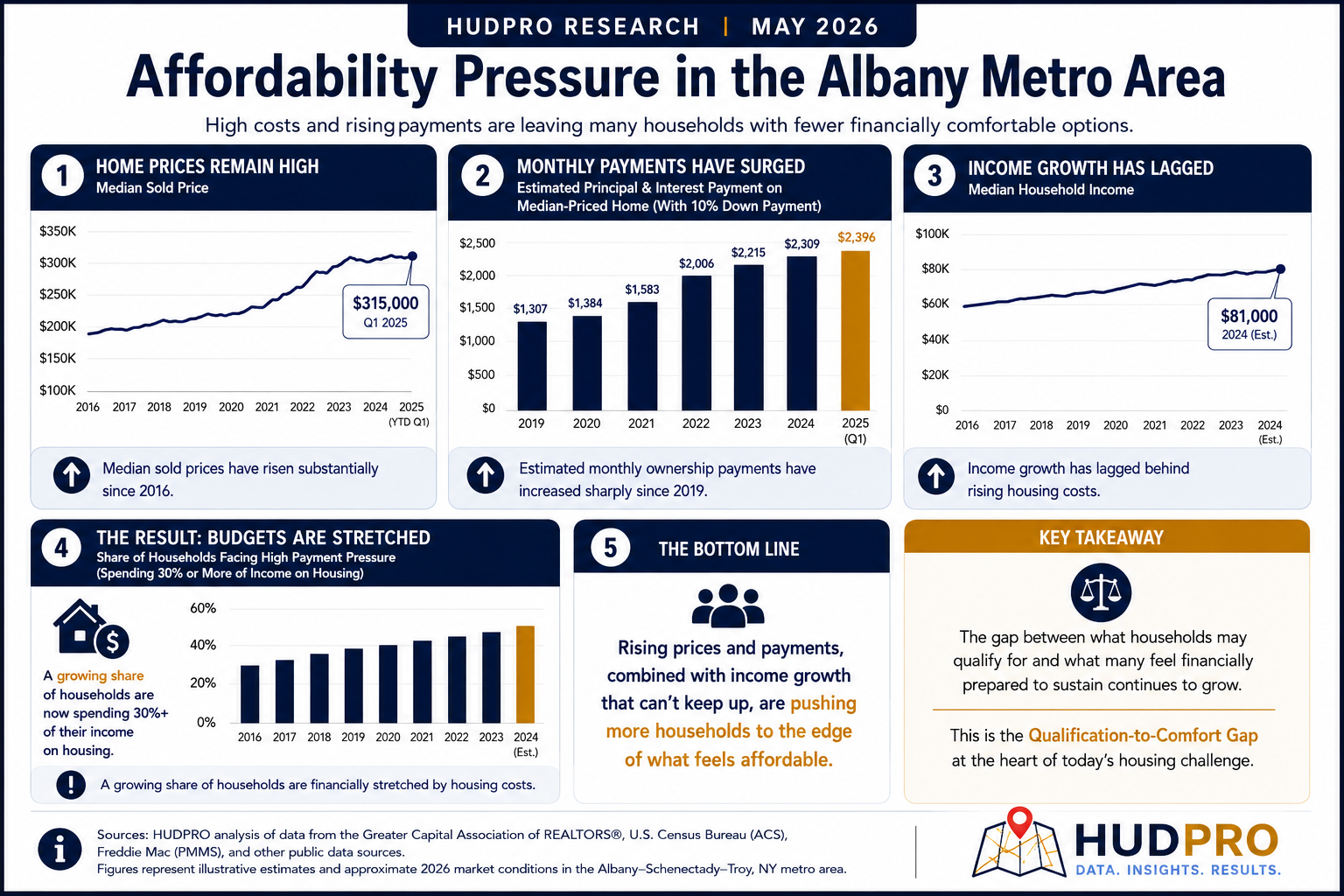

Compared with the low-rate environment of 2020–2021, today’s combination of higher mortgage rates, elevated taxes, insurance costs, and limited inventory has significantly increased the income needed to comfortably sustain ownership costs for new buyers entering the market.

This analysis reflects conditions facing new buyers entering today’s market, not homeowners who purchased years earlier under historically lower mortgage rates.

Primary affordability assumptions were derived from:

Historical context on Capital Region postwar housing development sourced from local historical research and town development records for Albany (Crestwood), Rotterdam (Cold Brook, Colonial Manor), and Troy (Sycaway, East Side / Albia expansion). The $120 billion federal housing subsidy figure for 1934–1962 reflects standard historical accounting in HUD and Census Bureau sources.

Active listing-price data was referenced separately as a market-pressure indicator rather than the primary affordability benchmark.

For the inventory channel data referenced in Where the missing inventory went, full sources are documented in HUDPRO’s companion study, A Quiet Pipeline, including HUD Single Family Production Reports (January 2022 through February 2026), HUD REO Portfolio Inventory data, Mortgagee Letters 2025-13 and 2026-03, and the 2026 HUD Office of Inspector General audit.

HUDPRO Research analyzes housing affordability, HUD home inventory trends, market accessibility, and buyer behavior across the United States. The goal is to translate complex housing data into clear, practical context for buyers making real decisions in today’s market.

Mike Belanger is a HUD-authorized real estate broker with nearly twenty years of experience and the founder of HUDPRO, a national HUD home intelligence platform based in Albany, New York.