How the houses ordinary American families used to buy stopped reaching them — and where they go now

HUDPRO Research Report | May 2026. Sources cited in article include HUD Single Family Production Reports, Mortgagee Letters 2025-13 and 2026-03, Urban Institute, GAO-19-228, HUD OIG, and others listed at the end of the piece.

I didn't set out to write this article. I set out to build a software platform.

For twenty years I sold HUD homes. I helped close to two hundred families buy a house that the federal government had foreclosed on, fixed almost nothing, and put back on the market at a price working people could afford. I watched buyers pick the wrong lender and lose the house at closing. I watched inspectors miss the burst pipes in a place that had sat empty through a Northeast winter. Then I built HUDPRO.

But once we started building, I started looking at the data. I had to. The platform needed it. And the more I looked, the less the data matched what HUD was telling the public.

In April, we published a piece on the rising wave of FHA foreclosures. In May, we published a study on Albany, New York, showing that a household with $107,000 in combined income — solidly middle-class — could qualify for a mortgage and still not afford the median home. That same week, we published an analysis of HUD's own monthly data showing FHA homebuyer activity had fallen 35% since October even as mortgage rates went **down**.

Each piece raised a question that led to the next one. By the time I sat down to write this, I had read fifty monthly FHA Single Family Production Reports spanning January 2022 through March 2026. I had read every Mortgagee Letter HUD has issued on foreclosure disposition since 2022. I had read a Government Accountability Office report from 2019, a comment letter from the National Community Stabilization Trust from 2020, an Urban Institute analysis from 2025, and the Mayer Brown legal analysis of the Senate bill that passed 89 to 10 in March 2026.

What follows is what I found. I am sharing my opinion only where I say I am. Everywhere else, I am telling you what the documents say.

— Mike Belanger, Founder, HUDPRO

You're probably making somewhere between $75,000 and $150,000 a year. Maybe you're a household of two earners. Maybe you have a kid in school. You watched friends and older siblings buy houses in 2008 and 2012 and 2014 that you couldn't buy today if your life depended on it. You've started to wonder if there's something wrong with you, or with your job, or with the choices you made in your twenties.

There isn't. The math broke. Here's how.

In 1947, William Levitt began building a development on Long Island. The houses were 950 square feet. Two bedrooms, one bath, no basement. They cost $7,990. The monthly payment was $58 — less than the rent on a two-bedroom apartment in New York City. By 1952, Levitt and Sons had built more than 70,000 of those houses and become the largest home builder in the United States.

What made the math work was not Levitt. It was federal policy.

The Federal Housing Administration, created during the New Deal, insured every loan written on a Levittown home. Before the FHA, a buyer had to put down more than half the purchase price in cash. After the FHA, 5% was enough. The GI Bill let returning veterans put nothing down on a thirty-year, government-backed mortgage. The Housing Act of 1948 made the FHA mortgage broadly available. Between 1934 and 1962, the federal government subsidized $120 billion in new housing — roughly $1.2 trillion in today's money.

This was, in the words of one historian, "the direct creation of U.S. government policy." The Truman administration faced a choice: build government-owned public housing for returning veterans, or subsidize private builders to put up privately owned houses for them. It chose the second. The mechanism was so generous and so broad that within a decade it built the American middle class.

One honest qualifier: that program was racially restricted by design. FHA underwriting redlined Black neighborhoods. Levittown's deeds barred non-white buyers. Only 2% of the $120 billion reached non-white households. The country has spent every decade since trying to undo the damage of that exclusion, and is still trying.

Housing professional with 23 years of experience in HUD-focused real estate and HUD-regulated housing workflows. About the author →

This article is HUDPRO editorial analysis. For external headlines, open Market News. By List is the live HUD inventory stats view; the map is where listings live.

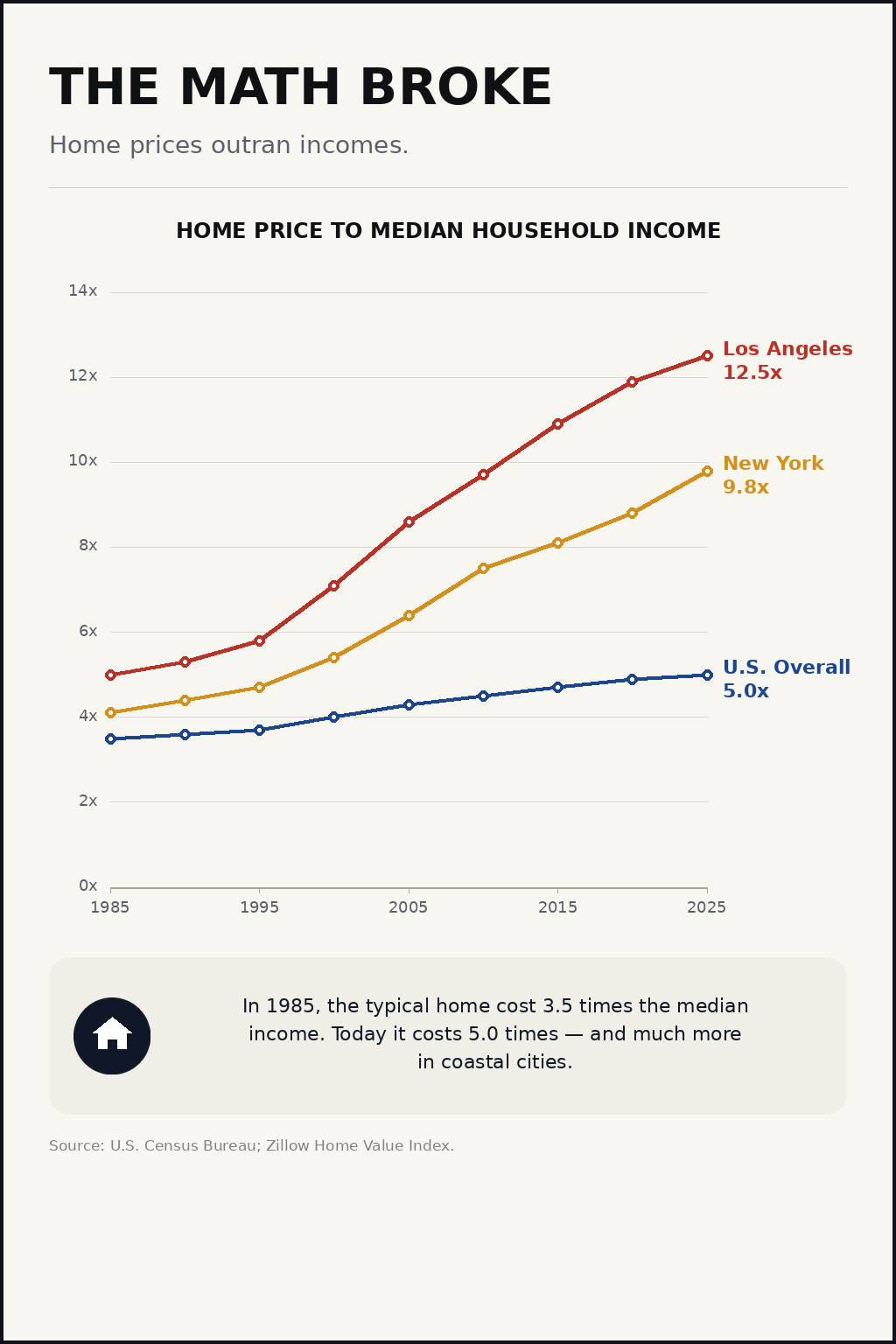

In 1985, the median American household earned $23,620. The median home cost $82,800. The ratio was 3.5.

In 2025, the median American household earns roughly $83,150. The median home costs $416,900. The ratio is 5.0.

For coastal markets, the ratio is much worse. In Los Angeles, the median home is 12.5 times the median household income. In New York, it is 9.8.

Home prices since 1985 are up roughly 408%. Median household income is up roughly 241%. If incomes and home prices had grown at the same rate over those forty years, today's median home would cost about $294,000 — roughly $122,000 less than it actually costs.

This is what economists call a divergence. What it means for you is simpler than that: the rule of thumb that your parents and grandparents used — buy a house that costs about three times your annual income — is no longer arithmetically possible in most of the country. The median home buyer in America is now 40 years old, up from 29 in the 1980s. People are waiting more than a decade longer to buy their first house because the math doesn't work any sooner.

So the question becomes: why?

There are a lot of explanations on offer. Low interest rates for too long. Zoning. Investor purchases. Demographic shifts. They all contain some truth. But none of them, by itself, answers the question of why the starter home — the small, simple, affordable house that used to be the entry point to the middle class — has nearly disappeared from new construction.

That answer requires looking at what builders actually decide to build, and why.

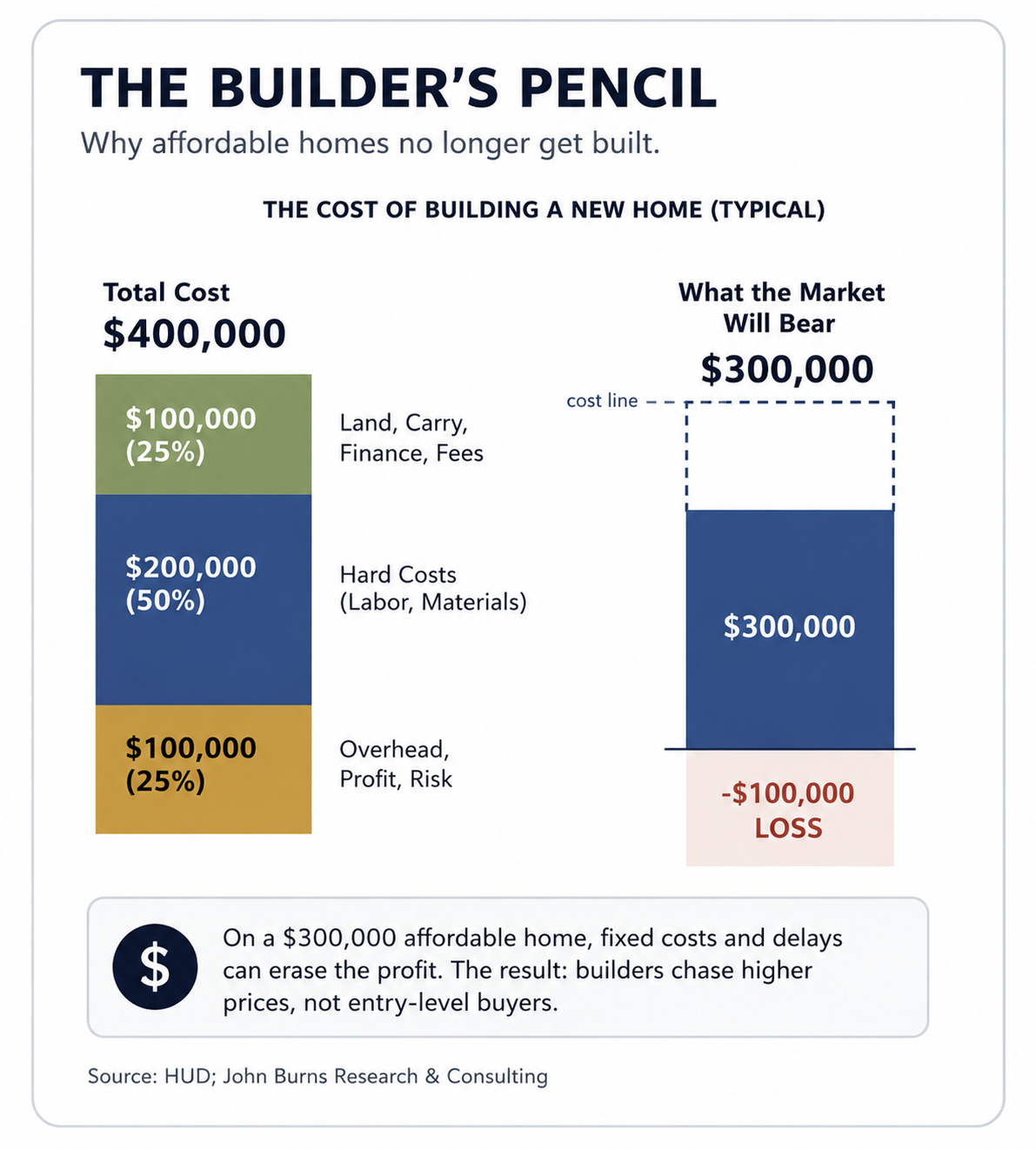

Builders are not villains in this story. They are running businesses. To understand why almost no one builds starter homes anymore, you have to understand the math the way a builder runs it on the back of a napkin.

Every house, regardless of size, carries a set of fixed costs that don't change much based on square footage. The building permit costs roughly the same. The sewer hookup costs roughly the same. The earth-moving, the management overhead, the architectural plans, the inspection schedule — all roughly the same whether the finished house is 1,200 square feet or 4,200 square feet. According to the National Association of Home Builders, 84% of builders in 2026 cite interest rates as their primary hurdle to building affordable inventory. The cost of borrowed money — the construction loan — runs on a clock whether the project takes four months or fourteen.

Now do the builder's math.

Build a $250,000 starter home and the margin might be 8% — about $20,000. If lumber prices spike, or a subcontractor walks off the job mid-project, or the permit office takes an extra ninety days to issue approval, that $20,000 evaporates. The builder loses money on the house.

Build an $800,000 home and the margin might be 20% — about $160,000. The same lumber spike, the same subcontractor walking, the same permit delay — and the builder still walks away with $130,000.

The builder didn't choose luxury because they prefer rich clients. They chose it because it was the only product that could survive the financial risk of getting built. The average new American home in 1955 was 950 square feet. The average new American home in 2024 was over 2,200 square feet. That difference isn't taste. It's the spreadsheet.

The result is that the entry-level housing supply — the thing the FHA was created to support — has been slowly removed from the new-construction pipeline. If you are looking for an affordable house in 2026, you are not looking at new construction. You are looking at existing homes.

And among existing homes, the most affordable category, by a wide margin, is distressed inventory.

When a homeowner with an FHA-insured mortgage falls far enough behind on their payments, a series of things happen. Most of them never make the news.

First, the loan servicer tries to work it out — loan modifications, forbearance, repayment plans. If that fails, the loan moves toward foreclosure. The borrower loses the house. The bank takes title back at a foreclosure auction. The bank then files a claim against the FHA insurance fund to recover its losses.

What happens next is the part you've probably always assumed worked one way. You'd assume — most Americans would — that the foreclosed house becomes a "HUD home," listed on the public HUD market, where regular working families can buy it with FHA financing of their own, often at a discount to market.

That's no longer what happens in most cases. And the reason it doesn't happen is that HUD itself does not want the property.

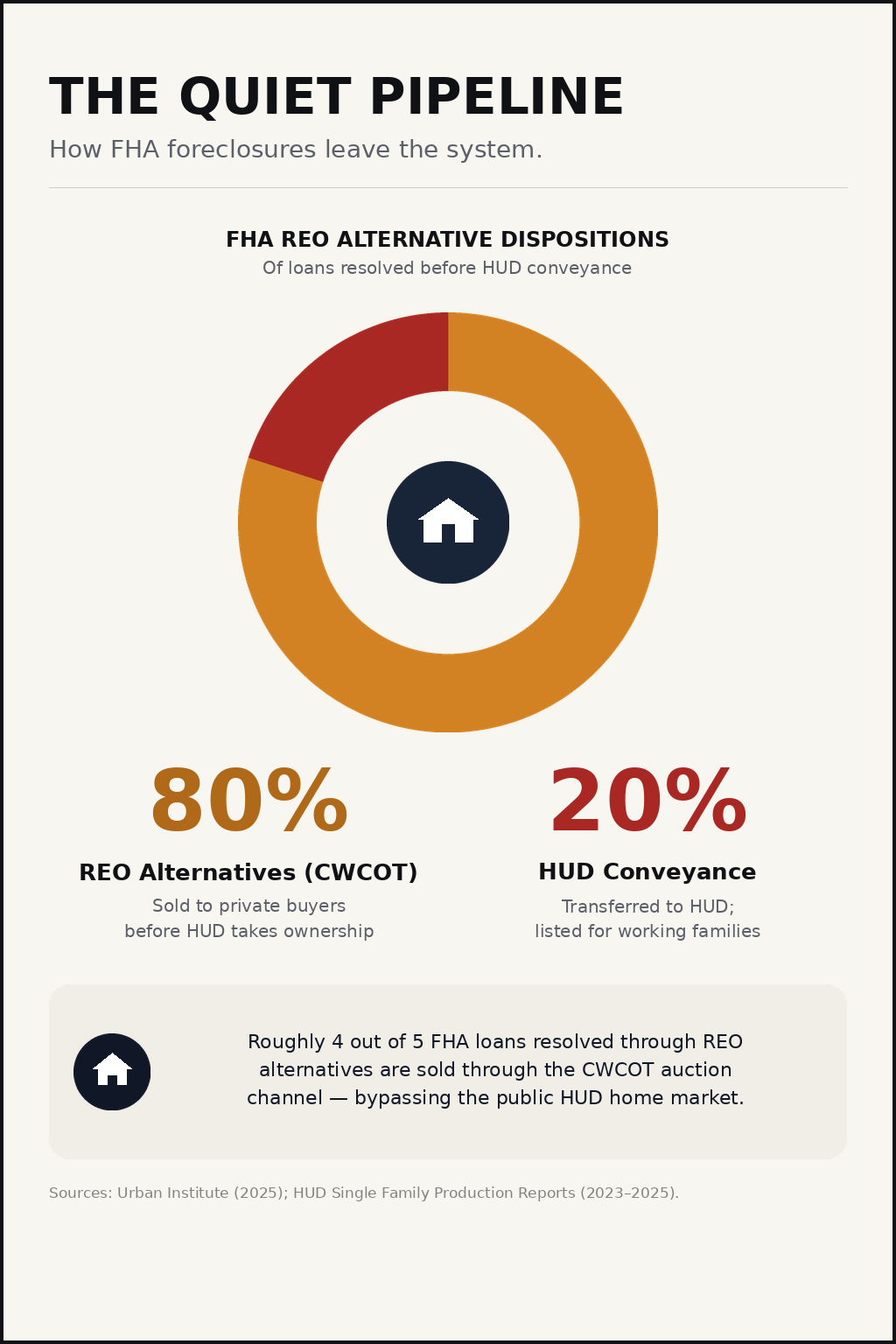

In 1987, HUD created a program called CWCOT — Claims Without Conveyance of Title. The phrase is bureaucratic, but the design is unmistakable. HUD pays the bank its insurance claim without taking title to the house. Instead, the bank is encouraged to sell the property to a third party — typically at a foreclosure auction or post-foreclosure online auction — and the bank pockets the auction proceeds. HUD then pays a claim covering the gap between the auction price and the loan balance. The property never reaches the public HUD market. HUD never owns it. HUD never has to maintain it, market it, or dispose of it. The bank gets made whole. The auction buyer gets the house.

The Urban Institute, in partnership with Auction.com, estimates that the CWCOT program has saved HUD's Mutual Mortgage Insurance Fund roughly $10 billion since 2012 compared to what HUD would have spent taking those properties into inventory and disposing of them traditionally.

That $10 billion in savings is the policy point. Conveyance costs more. Holding properties costs more. Marketing them to the public costs more. So HUD built a program that allows servicers to bypass HUD's inventory entirely, and HUD continues to tune that program — Mortgagee Letter after Mortgagee Letter — to make participation easier and more financially attractive for the servicers.

Here is a detail most Americans have never heard. Before the auction happens — and in many cases before the bank has even filed for foreclosure — HUD has already calculated the property's "Commissioner's Adjusted Fair Market Value," or CAFMV. The CAFMV is the floor: the price the property must sell for in order for the bank to qualify for an FHA insurance claim. The bank's authorized employees log in to FHA Connection, HUD's internal system, and look up the number. HUD calculates it by taking the property's "as-is" appraised value and subtracting adjustments based on the property's location, occupancy status, and appraised-value tier — adjustments meant to account for the holding and resale costs HUD would have incurred had it taken title. HUD does not publish the pricing matrix. HUD says only that it "regularly updates these adjustments based on market conditions." That phrasing is doing significant work. HUD is actively tuning the floor price for distressed FHA inventory, in real time, using a formula it has not disclosed. The bank has the number. The auction platform has the number. The ordinary buyer does not.

Here is what HUD's own monthly Single Family Production Reports show happened across the first quarter of 2026 — the three most recent months for which HUD has published data:

Roughly seven in ten FHA foreclosures sold through third-party channels. About two in ten reached the public HUD market through conveyance. The remainder resolved through short sale. The Urban Institute reports that CWCOT's share of FHA REO alternative dispositions has risen from 31% in 2012 to more than 80% in 2024.

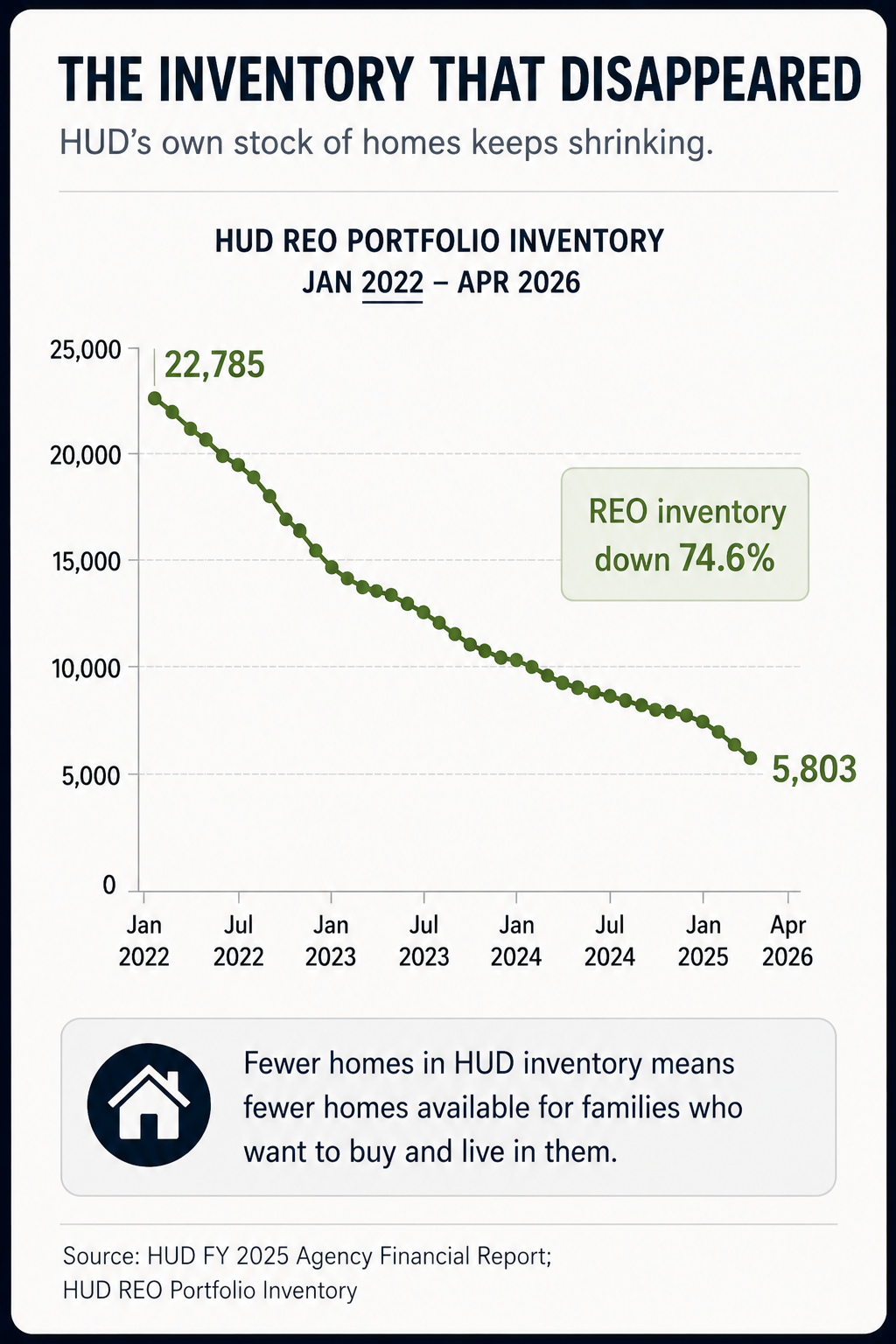

The number to remember is not 3,278. The number to remember is what's missing from the public HUD market as a result. Working families who were told their entry point to the housing market is HUD-owned inventory are looking at an inventory that, by design, contains a shrinking share of the houses that actually get foreclosed on in their county.

Looking at the full picture across 2023, 2024, and 2025, the pattern is more measured but no less significant. About 67% of all FHA foreclosure dispositions in those three years sold through third-party auction. Roughly 25% reached the public HUD market through conveyance. Roughly 8% resolved through pre-foreclosure short sales. Two out of every three FHA foreclosures never become a HUD home, by design. The first quarter of 2026 numbers above show that ratio holding — and tilting further toward the auction channel.

This is not a glitch in the system. The system is working exactly the way it was built to work. HUD did not close the pipeline. HUD turned the faucet down to a drip.

Auctions are not designed for working families. They are designed for capital.

To bid at most CWCOT-eligible foreclosure auctions, a buyer typically needs to bring a cash deposit on the day of the sale and pay the balance within hours to days of winning. There is usually no interior inspection allowed before the bid. The property may still be occupied. The title may have unresolved liens. Conventional and FHA financing — the kinds of mortgages working buyers actually qualify for — are almost impossible to use at this stage of the process.

What kinds of buyers thrive in that environment? Cash buyers. Buyers with pre-approved lines of credit from hard-money lenders. Buyers with legal departments to handle title issues, in-house renovation teams to handle deferred maintenance, and balance-sheet tolerance for properties that don't perform.

This is not a hypothetical. The Government Accountability Office, the Center for American Progress, the Center for Public Integrity, ProPublica, and the Center for Popular Democracy have all documented who has actually bought FHA distressed inventory at scale. Between 2010 and 2016, HUD sold roughly 111,000 non-performing FHA loans, worth $19 billion in unpaid principal balance, through a related program called the Distressed Asset Stabilization Program (DASP). According to a Center for American Progress analysis, 97% of those loans were purchased by private for-profit investors.

The largest buyer was Bayview Acquisitions, an investment vehicle 46% owned by Blackstone — the same private equity firm that became the largest single-family landlord in the United States during the same period. Bayview alone purchased nearly 24,000 FHA loans through the program, roughly 19% of the total. Other major buyers included Lone Star Funds, Oaktree Capital, and Selene Finance, later acquired by Pretium Partners. Each of these firms is now among the largest single-family residential investors in the country.

In 2019, the Government Accountability Office issued a report — GAO-19-228, requested by then-Representative Maxine Waters — confirming that the program needed significant reforms to protect borrowers and ensure the FHA disposition system was meeting its statutory purpose. The reforms were modest and partial.

The CWCOT auction is one of several channels through which distressed inventory reaches institutional investors. Before foreclosure, banks have historically bundled non-performing loans into portfolios and sold them directly to private equity firms and hedge funds — the channel that drove the original DASP program. After foreclosure, banks can bundle real-estate-owned properties into portfolios and sell them to single-family rental operators. Different mechanisms, same destination. CWCOT is the channel that has grown to dominate where FHA foreclosed homes end up, but the broader pattern of institutional capture has multiple paths.

One particular case is worth noting because the documentation is unusually complete. From 2009 to 2015, a California bank called OneWest was run by an investor group led by Steven Mnuchin. OneWest conducted approximately 36,000 foreclosures in California alone during this period. Its reverse-mortgage subsidiary, Financial Freedom, paid $89 million to the Department of Justice in 2017 to settle False Claims Act allegations that it had improperly extracted FHA insurance payments. Mnuchin's investor group sold OneWest in 2015 for $3.4 billion. Per Bloomberg's reporting, Mnuchin's personal payout was approximately $380 million.

Mnuchin then served as Secretary of the Treasury of the United States from 2017 to 2021. Joseph Otting, OneWest's former CEO, served as Comptroller of the Currency in the same administration.

I am not suggesting any specific quid pro quo. I am telling you what the public record contains, and noting that the people who profit most from the FHA disposition system often operate within the financial and regulatory institutions surrounding it.

To make this concrete, imagine a household.

You are two adults in your early thirties living in Indianapolis. She teaches second grade in Marion County and earns $52,000. He works for a county maintenance department and earns $38,000. Combined, you make $90,000 — a comfortable middle-class household income on paper.

You have $18,000 in savings, which is enough for a 3.5% FHA down payment on a house up to about $400,000, plus closing costs. You both have credit scores in the 680s. You have one young child and another on the way. You have been pre-approved by a lender who has done a few FHA deals before. You have been watching the housing listings for the better part of a year.

In the Indianapolis MSA in early 2026, the median home price is roughly $260,000. Even at that median, the math is tight. Your front-end debt-to-income ratio at the median home, with current rates, taxes, and FHA mortgage insurance, runs close to 32% — above the conventional 28% guideline. You are looking, in practice, at homes priced $230,000 and below. There aren't many of those, and the ones there are tend to need work.

A HUD home priced at $185,000 — needing a new roof, with the standard 203(k) renovation loan added in to bring it to liveable — would be exactly the kind of property that put a family like yours into homeownership in 2009, or 2014, or 2018. According to HUD's March 2026 Production Report, only 0.5% of FHA buyers nationally used 203(k) financing that month. Not because the program doesn't exist. Because the inventory has thinned, and the buyers and lenders who used to be familiar with how it worked have moved on.

So you keep watching listings. You check the public HUD listings occasionally — or platforms like HUDPRO.com that aggregate them. You don't see much. You don't realize that for every house that reaches the public HUD market from your county, four others have already been sold at auction, to buyers you've never heard of, on platforms you don't have access to.

You don't know any of this because no one has told you.

The policy direction over the past few years has not corrected the structural problem. It has accelerated it.

In April 2025, FHA issued Mortgagee Letter 2025-13. The letter eliminated a thirty-day exclusive sales period that had been created in 2022 to let owner-occupants, nonprofits, and government entities bid on FHA foreclosure properties before investors could. It also reverted a thirty-day exclusive listing period on HUD-conveyed properties back to fifteen days. HUD's stated justification was that the prior exclusive periods had produced "mixed results at best" — that "very few Properties have sold to Owner-Occupant Buyers" during the protected windows. The implementation deadline was May 30, 2025.

In January 2026, FHA issued Mortgagee Letter 2026-03. This one is less widely understood. It required loan servicers to bid the property's Commissioner's Adjusted Fair Market Value at foreclosure sale in order to qualify for CWCOT claims. It eliminated the small-servicer exemption that had previously allowed smaller servicers to opt out. And it added a financial incentive: HUD now reimburses servicers 100% of any amount they pay over the credit bid to reach the required value. In effect, HUD is now directly subsidizing servicers to push more inventory through the CWCOT channel rather than convey it to the public market. Implementation deadline: April 29, 2026.

And there is one more piece of evidence the public should know about. In 2026, the HUD Office of Inspector General released an audit finding that HUD had paid claims from the Mutual Mortgage Insurance Fund — the same fund the CWCOT program is said to save — for an estimated 239,000 properties for which lenders had missed foreclosure and conveyance deadlines. Over a five-year period, the OIG estimated, those delays cost the fund $141.9 million in unnecessary interest and $2.09 billion in unnecessary holding costs. The savings claim cuts both ways.

In March 2026, the U.S. Senate passed the 21st Century ROAD to Housing Act by a vote of 89 to 10. The White House announced strong support. The bill includes a temporary ban on large institutional investors purchasing single-family homes — the most aggressive federal action on institutional housing ownership in a generation.

The bill contains exceptions. One of them: institutional investors are still permitted to purchase single-family homes acquired through foreclosure, deed-in-lieu, enforcement of security interest, or loss mitigation. The exact pathway that distressed FHA inventory now flows through.

This is the mechanical reason the broader bill may fail its own stated objective. If you ban institutional investors from buying homes on the open market but leave the foreclosure pipeline open — and the foreclosure pipeline is already the channel through which most distressed inventory passes — then institutional investors will simply pivot more aggressively into the channel that is still open. The bill restricts the front door of the institutional acquisition system while leaving the back door wide.

In January 2026, the Trump administration also issued an Executive Order targeting private equity ownership of single-family homes and setting the stage for antitrust enforcement against institutional landlords. The Order addresses the holding side of the institutional pipeline. It does not address the acquisition side — meaning it does not change how FHA distressed inventory reaches institutional buyers in the first place.

Both political parties are now publicly concerned about institutional investor ownership of American housing. Neither has yet acted on the foreclosure pipeline that feeds it.

There is a serious counter-argument to this piece, and you should hear it directly.

In June 2025, the Urban Institute, in partnership with Auction.com (which operates more than half of all CWCOT auctions in the United States), published an analysis arguing that the CWCOT program produces better owner-occupancy outcomes than the alternative. Their headline findings: 73% of renovated CWCOT resales are owner-occupied, twelve percentage points higher than the rate for traditional HUD-conveyed properties. CWCOT properties return to market roughly 466 days faster than properties that go through traditional conveyance. The program has generated over $705 million in surplus funds for distressed homeowners, averaging about $38,000 per surplus-generating sale.

These findings are real and should not be dismissed. They suggest that, viewed at the level of eventual ownership, properties passing through CWCOT often do end up with owner-occupants.

But there is a layer the headline numbers obscure. The 73% figure measures renovated resales — properties bought at auction by an investor, renovated, then resold to an owner-occupant. The owner-occupant in that transaction is not the buyer at the auction. The investor is. The owner-occupant arrives later, paying a price that incorporates the investor's profit margin.

That is not the same thing as direct owner-occupant access to distressed inventory. It is owner-occupant access with an investor middleman taking a profit layer. For the household I described in section six, the difference is the difference between buying a house for $185,000 plus repairs and buying the same house for $245,000 already renovated. One is a path to homeownership for a middle-income household. The other is a path that requires the household to fund the investor's margin.

Urban Institute and Auction.com would likely point out, correctly, that the alternative — properties sitting vacant for hundreds of days while deteriorating in HUD inventory — is also not good for owner-occupants. They are not wrong. But "the alternative is worse" is a different claim than "the current system serves owner-occupants well."

This is the only section of this article where I am going to share an opinion. I am not a policy maker. I am someone who has spent twenty years inside this market.

Let me state the obvious that nobody seems willing to state. Between 1934 and 1962, the federal government chose to invest, in then-current dollars, $120 billion in expanding American homeownership. That program was racially restricted by design, and the country has spent every year since trying to undo that part. But the mechanism — federal insurance backing affordable mortgages, federal coordination of housing supply at scale, federal policy treating working-family homeownership as a national priority worth public dollars — was the most successful housing intervention in American history. It built the middle class.

That apparatus still exists. The FHA still exists. The 203(k) rehabilitation loan still exists. HUD's asset management contractors still exist. The HUD Homes program still exists. None of it was abolished. It was simply, over decades, quietly redirected.

The country is now in a housing crisis comparable in scale to the one HUD was created to solve in 1934. Working families cannot afford new construction because builders cannot afford to build affordable houses. Working families cannot access distressed inventory because four out of every five FHA foreclosures now bypass the public market — most through investor auction. The entry point to American homeownership — the thing the federal government once built deliberately and at scale — has been quietly closed.

The simplest move on the table is this: reverse the current split.

In the first quarter of 2026, 3,278 FHA foreclosures sold through third-party auction. 905 were conveyed to HUD and entered the public market. Across 2023-2025, the average ratio was two-to-one: two FHA foreclosures sold through third-party channels for every one that reached the public HUD market. In Q1 2026, that ratio widened to roughly three-and-a-half to one. If even half of those auction properties had instead been routed through HUD conveyance, the public inventory available to working buyers that quarter would have nearly tripled. Imagine 1,000 additional HUD homes entering the public market every month, every county, every state. That is not a hypothetical. That is what the data shows would happen under a different policy choice.

HUD's stated reason for routing properties away from conveyance is that conveyance is too slow. The Urban Institute found that the traditional HUD process — taking properties into inventory, maintaining them, and reselling them through the public market — takes 466 days longer than CWCOT. That gap is real, and it is the policy lever HUD has used to justify the entire CWCOT expansion. But 466 days is not a law of physics. It is the result of an organization that has not been given the resources or the political mandate to move faster. Private investors are not 466 days faster than HUD because they are geniuses. They are faster because they are funded, staffed, and focused on speed. HUD could be too. HUD has chosen not to be.

The fix is not technically difficult. HUD's asset management contractors already exist. The infrastructure to handle conveyed inventory already exists. What is missing is the political decision to fund it adequately, route more inventory through it, and treat working-family access to the public HUD market as the program's primary purpose rather than a residual outcome.

This would not be a revolution. It would be a restoration. It would not require new legislation. HUD has the administrative authority to reverse most of what the past three years of Mortgagee Letters have done. The Senate could close the foreclosure carve-out in the 21st Century ROAD to Housing Act when it comes up for amendment. The administration could issue an Executive Order on the acquisition side of the institutional-investor pipeline to match the one it has already issued on the holding side.

None of this is the full solution. The builder's pencil problem in section three is not solved by routing more foreclosed houses to HUD. The 5-to-1 home-price-to-income ratio is not solved by any single intervention. But the federal government showing that it is willing to redirect even one piece of the housing-access pipeline back toward the families it was originally built to serve — that would be a sign of good faith. A demonstrable, measurable, achievable starting point.

It is the simplest thing the government could do. It is currently doing the opposite.

I want to take you back to Indianapolis.

The couple I described in section six is not a real couple. But the household they represent is real, and there are millions of them. The teacher earning $52,000. The maintenance worker earning $38,000. The $18,000 in savings. The pre-approval letter. The Zillow searches at the kitchen table after the kids go to bed.

In 1948, a couple with that exact income profile — adjusted for inflation, adjusted for the work each of them does — would have been the precise target buyer of the FHA's signature program. The federal government would have insured their mortgage. The GI Bill would have backstopped their down payment. The Levitts of the world would have been building houses priced at three times their combined income. The math would have worked. Their children would have grown up in a house they owned.

That couple in 2026 is doing nothing differently than the couple in 1948. The teaching certificate took the same effort. The county job pays in proportion to the work. They saved at the same diligence. The thing that has changed is not them. The thing that has changed is the system that used to deliver houses to families like theirs.

They do not know that the house they would have bought — the small, distressed, fixable house that used to be the entry point to the middle class — has been quietly routed away from them by a program HUD itself designed and continues to optimize. They do not know that four out of every five FHA foreclosures in their county now get sold off-market, in channels they cannot access, paid for in part by a federal insurance fund their taxes support. They do not know that the bill the Senate just passed by 89 votes to 10 contains an exception that keeps the pipeline pointed away from them.

They do not know any of this because no one has told them.

I built HUDPRO to help working families buy HUD homes. What I have learned in building it is that the problem is larger than the platform can solve on its own. The pipeline is being narrowed by people who are not in the room when working families are deciding whether to keep saving or to give up.

You are not the couple in Indianapolis. But you know one. You may be married to one. You may have raised one. You almost certainly went to high school with one. The system that excluded their parents from the postwar housing boom was a system the country eventually noticed and tried to fix. The system that is excluding their children was built so quietly that almost no one has noticed it is happening.

That part is on us. The data is in HUD's own monthly reports. The mechanism is in HUD's own Mortgagee Letters. The beneficiaries are documented in court filings and SEC disclosures. The policy fix is in front of Congress right now and was already debated in March.

You have two senators and a member of the House. They take constituent calls. They especially take calls from people who can name a specific bill, a specific section, and a specific reason it matters. The bill is the 21st Century ROAD to Housing Act. The section is the institutional-investor exception. The reason it matters is the couple in Indianapolis.

You don't know any of this because no one has told you.

Now you know.

Mike Belanger is a HUD-authorized real estate broker with nearly twenty years of experience and the founder of HUDPRO, a national HUD home intelligence platform based in Albany, New York.

HUD Single Family Production Reports, January 2022 through February 2026 (49 reports total). HUD.gov.

HUD Office of Inspector General, "FHA Paid Claims for an Estimated 239,000 Properties That Servicers Did Not Foreclose Upon or Convey on Time," 2026.

HUD FY 2025 Agency Financial Report, U.S. Department of Housing and Urban Development, December 2025.

HUD Real Estate Owned (REO) Portfolio Inventory, monthly inventory data, January 2022 through April 2026.

Mortgagee Letter 2025-13, U.S. Department of Housing and Urban Development, April 28, 2025.

Mortgagee Letter 2026-03, U.S. Department of Housing and Urban Development, January 29, 2026.

Government Accountability Office, "Federal Housing Administration: Opportunities Exist to Improve Defaulted, Single-Family Loan Sales," GAO-19-228, March 2019.

Urban Institute, "How the CWCOT Program Could Deliver Even More Benefits to the FHA, Borrowers, and Homeowners Facing Foreclosure," June 2025.

National Community Stabilization Trust, Comment letter on CWCOT program, March 2020.

Center for American Progress, analyses of DASP buyer composition, 2014-2016.

Center for Public Integrity, "Hedge funds get cheap homes, homeowners get the boot," 2015; coverage of DASP program scrutiny, 2016.

ProPublica, "Trump's Treasury Pick Excelled at Kicking Elderly People Out of Their Homes," November 2016.

Mayer Brown, "US Senate Advances Housing Legislation that Includes a Ban on Institutional Investors Purchasing Single-Family Homes," March 27, 2026.

Foley & Lardner, "New Executive Order Focuses on Private Equity Ownership of Single-Family Homes and Sets Stage for Antitrust Enforcement Action," January 23, 2026.

National Association of Home Builders, 2026 builder sentiment data.

Federal Reserve Bank of St. Louis (FRED) and Motio Research, U.S. home price-to-income ratio data, 1985-2025.

Statista, "House Prices Outpaced Income Growth Over the Past 40 Years," 2024.

Levittown historical figures verified against multiple sources including Yale University Press, Lincoln Institute of Land Policy, NYU Institute of French Studies, and the National Association of Housing Cooperatives.

Mnuchin / OneWest figures verified against Bloomberg, NBC News, ABC News, HousingWire, and U.S. Department of Justice settlement records.