The Operating Manual · Education

FHA Financing for HUD Homes:

Which loan fits your property?

Most HUD buyers do not need the same FHA loan. Your HUD case status — ININInsurable. A HUD case-status code generally indicating the property meets FHA minimum property standards and qualifies for standard 203(b) financing., IEIEInsurable with Escrow. A HUD case-status code generally indicating the property has limited required repairs that can be addressed through a repair escrow at closing under 203(b)., or UIUIUninsurable. A HUD case-status code generally indicating the property does not currently qualify for standard FHA 203(b) financing without rehabilitation work — often a candidate for 203(k). — usually points to the correct financing path.

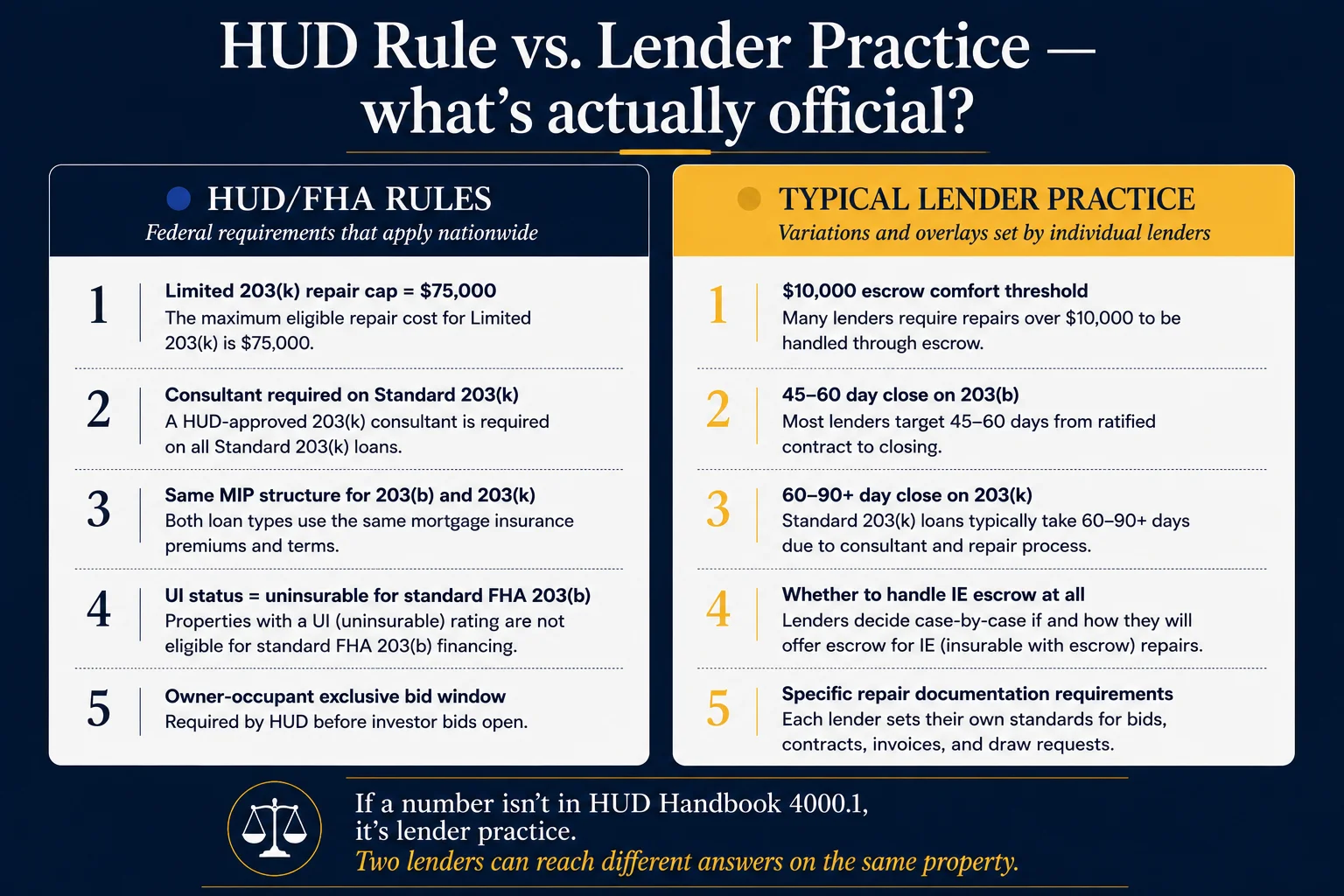

Some thresholds in this guide are HUD rules; others are typical lender practice. We mark which is which.

- Eligibility

- Owner-occupants and qualified buyers using FHA-insured financing

- Common timeline range

- 45–60 days for 203(b) · 60–90+ days for 203(k)

- Max repair limit (financed)

- Limited 203(k): up to $75,000 · Standard 203(k): no program cap (subject to FHA loan limits)

Step 1 — Find your property's code

Match the HUD case status to the FHA loan path.

Every HUD listing carries a case-status code that tells FHA buyers what financing usually fits. The code is the fastest way to know what loan to plan around before you submit a bid.

- Standard FHA financing

- Property generally meets FHA standards

- Most common owner-occupant path

- Most close in 45–60 days

- Limited required repairs

- Escrow typically held at closing

- Repairs completed post-close

- Still a 203(b) loan structurally

- More extensive repair scope

- Renovation financed into loan

- 203(k) is the usual FHA option, not the only path

- Longer timeline (60–90+ days typical)

FHA 203(b) is the basic FHA mortgage insurance program for buying a primary residence.

FHA 203(k) is the rehabilitation version — same FHA insurance structure, but the loan also finances repair work.

Step 2 — Compare the paths side-by-side

One table. The whole decision.

How each status typically translates into loan structure, repair handling, and timing. Cells marked with a navy dot are HUD or FHA rules. Cells marked with a gold dot are typical lender practice and may vary.

| HUD case status | Typical FHA path | Repair scope | Repair escrow? | Consultant required? | Typical timeline | Complexity | Most common buyer mistake |

|---|---|---|---|---|---|---|---|

| IN — Insurable | 203(b) | None or minimal | Usually no | No | 45–60 days | Low | Assuming any HUD home requires 203(k) |

| IE — Insurable w/ Escrow | 203(b) with repair escrow | Limited, lender-dependent | Yes — held at closing | No | 45–60 days | Low–Medium | Confusing repair escrow with a HUD grant |

| UI — Uninsurable | 203(k) Limited or Standard | Larger or structural | N/A — repairs financed into loan | Standard: typically yes • Limited: typically no | 60–90+ days | Medium–High | Assuming UI means the home is unlivable |

Step 3 — Translate the codes

What these codes actually mean for the buyer.

Most pages on the internet stop at definitions — “UI means uninsurable” — and move on. That is not enough. What buyers need is the operational meaning.

A property the appraiser believes meets FHA standards as-is. The financing conversation is usually a standard 203(b) loan — same as buying any FHA-eligible home, just in the HUD inventory.

A property with limited required repairs the lender is willing to handle through escrow. The buyer still uses 203(b); the repair money is part of the loan, held at closing, and released after the work is verified post-close.

A property that does not currently qualify for standard 203(b) financing without rehab work. UI does not mean the home is condemned, unlivable, or worthless. It means an FHA buyer typically needs 203(k) — or a non-FHA loan — to make the purchase work.

The case-status code is a financing-eligibility signal, not a quality verdict. A UI property may be perfectly livable — it just needs more work than a standard 203(b)203(b)The standard FHA home mortgage loan for purchasing or refinancing a principal residence. The default FHA path for most HUD home buyers. loan can handle on its own. A house priced low and coded UI is not automatically a bad house; it is a house that needs the right loan.

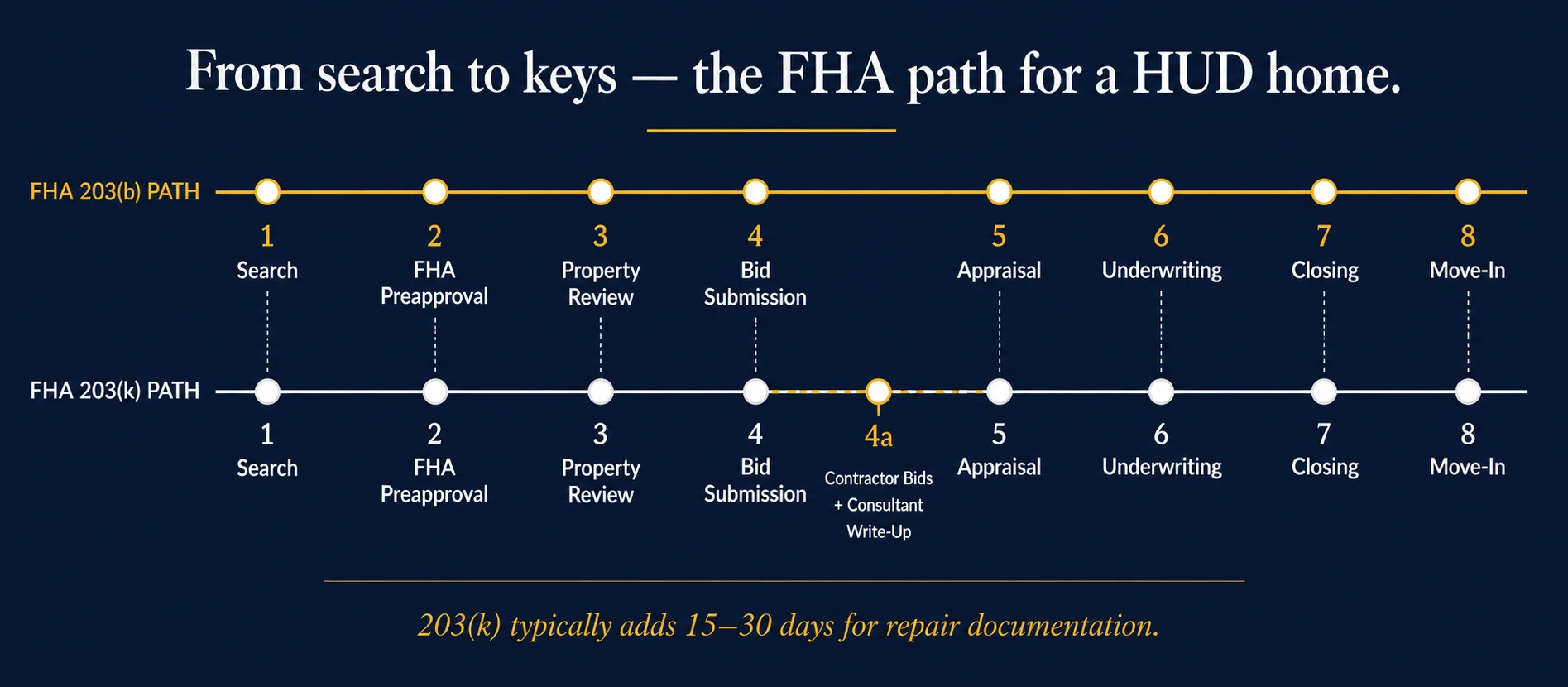

Step 4 — The buyer workflow

From search to keys: the actual sequence.

The sequence is the same whether you end up on 203(b) or 203(k). What changes is the level of documentation, the timeline, and whether a consultant is involved.

- 01

Search

Identify HUD-listed properties matching your area, price, and occupancy goal.

- 02

FHA Preapproval

Get preapproved with a lender that handles 203(b) AND 203(k). Many lenders only do one.

- 03

Property Review

Check the listing's case status code (IN, IE, UI) before deciding what loan path to plan for.

- 04

Status Interpretation

Match the code to the likely FHA path. Confirm with your lender — they hold the final call on which program works.

- 05

Bid Submission

HUD bids run on owner-occupant priority windows. Submit through a HUD-authorized broker.

- 06

Contractor Bids (UI only)

For 203(k), gather contractor bids and (for Standard 203(k)) a consultant work write-up before underwriting.

- 07

Appraisal

FHA appraisal flags any new property-condition issues. Surprises here can shift the loan path.

- 08

Underwriting

Lender finalizes loan structure. 203(b) is faster; 203(k) requires repair documentation review.

- 09

Closing

Loan funds. For IE properties, the repair escrow is established. For 203(k), the rehab account is funded.

- 10

Repairs & Move-In

IE repairs completed post-close within the lender's window. 203(k) work begins per the consultant's draw schedule.

Step 5 — Avoid these

Five mistakes that derail HUD buyers.

These come up in roughly that order — from the moment a buyer first sees a HUD listing through the closing table.

Assuming UI means the home is condemned

UI is a financing-eligibility code, not a property-quality verdict. Many UI homes are perfectly livable — they just need work that exceeds what 203(b) can handle.

Confusing repair escrow with a HUD grant

The escrow money is part of your loan. You borrow it, it sits in escrow at closing, and the work gets verified after. It is not free money from HUD.

Believing $10,000 is the magic line between 203(b) and 203(k)

That number gets repeated everywhere, but it is not a HUD rule. Some lenders use it as an internal guideline. The real decision depends on the specific repair issues, FHA Minimum Property Standards, and the lender's overlay.

Choosing a lender who only does 203(b)

If the property's case status shifts during appraisal — or you change your mind on scope — you may need 203(k). A lender who handles both gives you optionality.

Underestimating the 203(k) timeline

Standard 203(k) routinely takes 60–90+ days. Buyers who plan for a 30-day close on a UI property often blow up their own deal.

From the HUDPRO Field

What 20 years of HUD sales actually teaches you.

The single hardest pattern to break with HUD buyers is the belief that the case-status code is a verdict on the property. It is not. It is a verdict on the loan.

On a typical UI listing, I have watched buyers walk away from homes that needed twelve to twenty thousand dollars of work — work that 203(k) Limited handles cleanly — because the code scared them, or because their lender only does 203(b) and never mentioned the alternative. The house was fine. The match was wrong.

The fix is almost always upstream: find a lender who handles both programs before you start writing offers. A lender who can move between 203(b) escrow and 203(k) Limited without friction lets you bid on a much wider slice of the HUD inventory. Many buyers never realize how much their options expand when their lender can handle both paths.

FAQ

What buyers ask before they bid.

Sources & Notes

How this page separates HUD rules from buyer guidance.

HUDPRO is an independent buyer-education platform. We are not the originator of FHA loans, and we are not the official HUD listing authority. This page summarizes program rules from official HUD and FHA sources, and adds operational interpretation drawn from 20+ years of broker experience handling HUD-owned inventory.

- FHA 203(b) — Federal Housing Administration single-family mortgage insurance program. See HUD Handbook 4000.1.

- FHA 203(k) — Rehabilitation Mortgage Insurance program (Limited and Standard). HUD Handbook 4000.1, Section II.A.8.

- Limited 203(k) repair cap — currently $75,000 following HUD's 2024 program update.

- MIP — 1.75% upfront premium and an annual premium, applied identically to 203(b) and 203(k).

- Consultant fees — figures cited reflect HUD's updated 203(k) consultant fee schedule. Final fees vary by project scope and consultant.

This page is general buyer education. It is not lending advice, tax advice, or a substitute for the guidance of a licensed FHA lender, real estate broker, or HUD-approved counselor. FHA program rules and lender overlays change over time. Confirm current requirements with your lender and consult official HUD program documentation before making a financial decision.