Is FHA Drifting Away From Its Original Homeownership Mission?

Sources include HUD’s January 2026 FHA Single Family Production Report; FY2025 FHA first-time buyer statistics cited by HUD; FHA Mortgagee Letters 2025-13 (April 2025) and 2026-03 (January 2026). HUDPRO Research, May 2026.

Most people think they understand how a HUD Home works.

Somebody loses a house.

The government takes it back.

Then it shows up online, where ordinary people finally get a chance to buy it.

Simple enough.

Except that is not what is happening anymore.

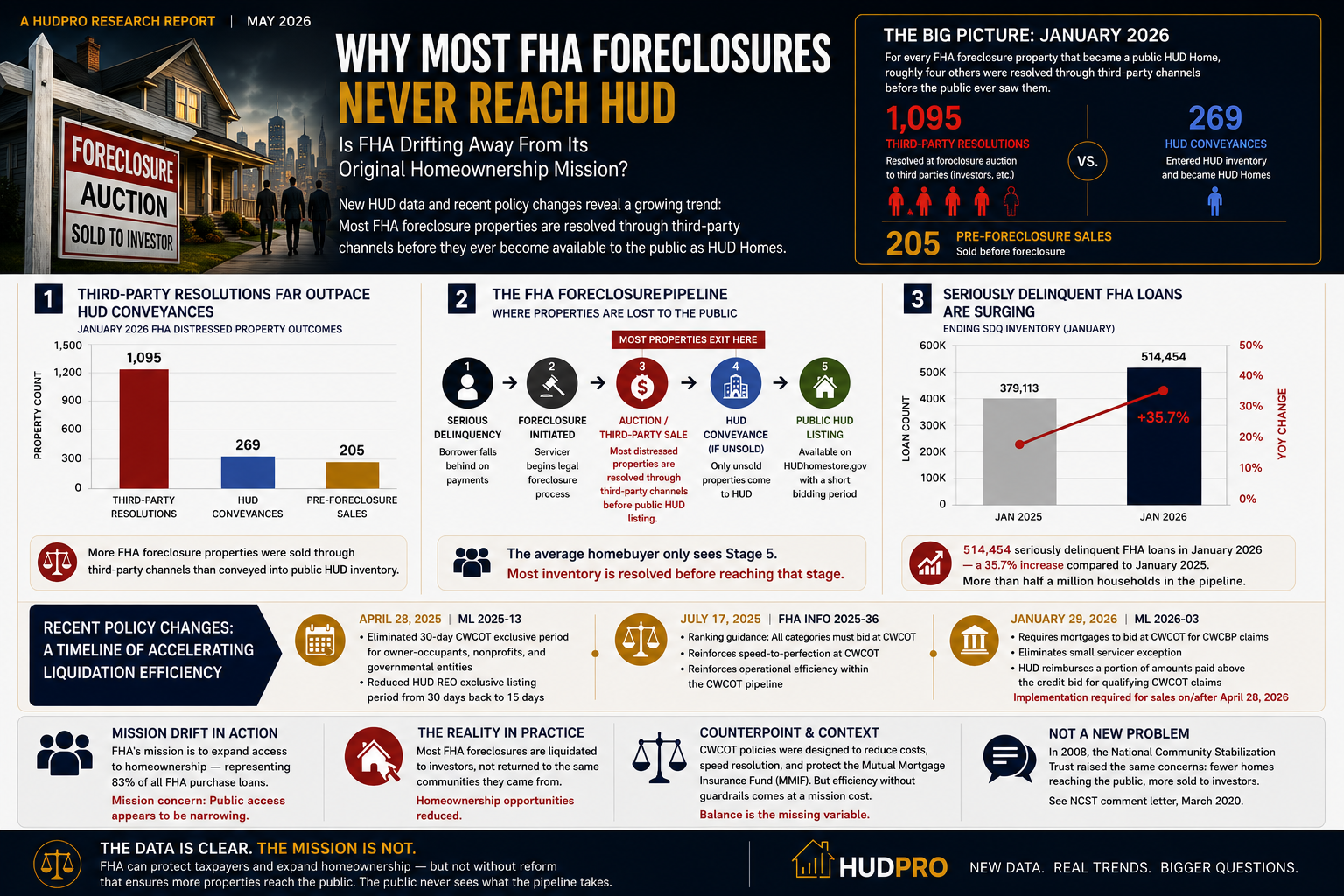

According to HUD’s own January 2026 numbers, for every FHA foreclosure property that became a public HUD Home, roughly four others were sold off before the public ever saw them.

Not hidden.

Not secret.

Just gone earlier in the process.

And if you are an ordinary buyer sitting at your kitchen table searching for an affordable home, you are mostly seeing what is left behind.

That is the part almost nobody talks about.

A HUDPRO Research Report — May 2026

When people talk about the housing crisis, they usually talk about what is visible.

High prices.

High interest rates.

Low inventory.

Bidding wars.

But there is another part of the market most people never see.

It exists before the “For Sale” sign.

Before the online listings.

Before the public bidding period.

And increasingly, that is where many FHA foreclosure properties disappear.

HUD’s January 2026 FHA Single Family Production Report showed:

In plain English:

For every FHA foreclosure property that became a public HUD Home, about four others were resolved before ordinary buyers ever got a realistic chance to purchase them.

Housing professional with 23 years of experience in HUD-focused real estate and HUD-regulated housing workflows. About the author →

This article is HUDPRO editorial analysis. For external headlines, open Market News. By List is the live HUD inventory stats view; the map is where listings live.

Most people imagine foreclosure as a straight line.

Someone loses the house.

The government takes it back.

The public gets a chance to buy it.

But real life is messier than that.

Long before a property reaches public inventory, another world opens up around it:

That world moves fast.

Ordinary buyers usually do not.

Most families are trying to:

Meanwhile, many distressed properties are already moving through an earlier pipeline most consumers never participate in.

That is why one line in this story matters more than anything else:

By the time many people begin searching for affordable homes, much of the inventory has already passed through earlier channels.

And those earlier channels often favor:

Not ordinary financed buyers.

Foreclosure auctions are not designed for first-time homebuyers.

They are built for people who know how the system works.

Some properties require:

For investors, that can be opportunity.

For ordinary buyers, it can feel impossible.

A teacher.

A nurse.

A young family.

Most are not walking into courthouse auctions with certified funds and renovation budgets.

And that matters because more FHA properties now appear to be resolving at those earlier stages.

Not after public listing.

Before it.

In April 2025, HUD issued Mortgagee Letter 2025-13.

The change reduced certain owner-occupant protections tied to FHA foreclosure disposition timelines.

Then in January 2026, HUD issued Mortgagee Letter 2026-03, reinforcing portions of the third-party foreclosure resolution process and tightening bidding requirements tied to CWCOT claims.

The language was technical.

But the direction was not.

The system appears increasingly focused on:

None of those goals are inherently wrong.

But they do raise a larger question:

Because FHA was not originally created to simply liquidate distressed properties quickly.

It was created to expand homeownership.

Especially for ordinary Americans.

Especially for first-time buyers.

This is where the numbers become difficult to ignore.

In FY2025:

That is FHA’s public-facing mission.

But on the foreclosure side, many of those same buyers are effectively shut out before properties ever reach the public market.

The contradiction is hard to miss.

Supporters of the current system correctly point out that many distressed homes eventually return to the market after renovation.

And that is true.

But by then, the economics are often completely different.

A property that may once have represented an affordable entry point for a first-time buyer can reappear months later with:

The house may still exist.

That is the deeper concern behind the numbers.

Because this is not simply about whether homes return to the market.

It is about who can still afford them when they do.

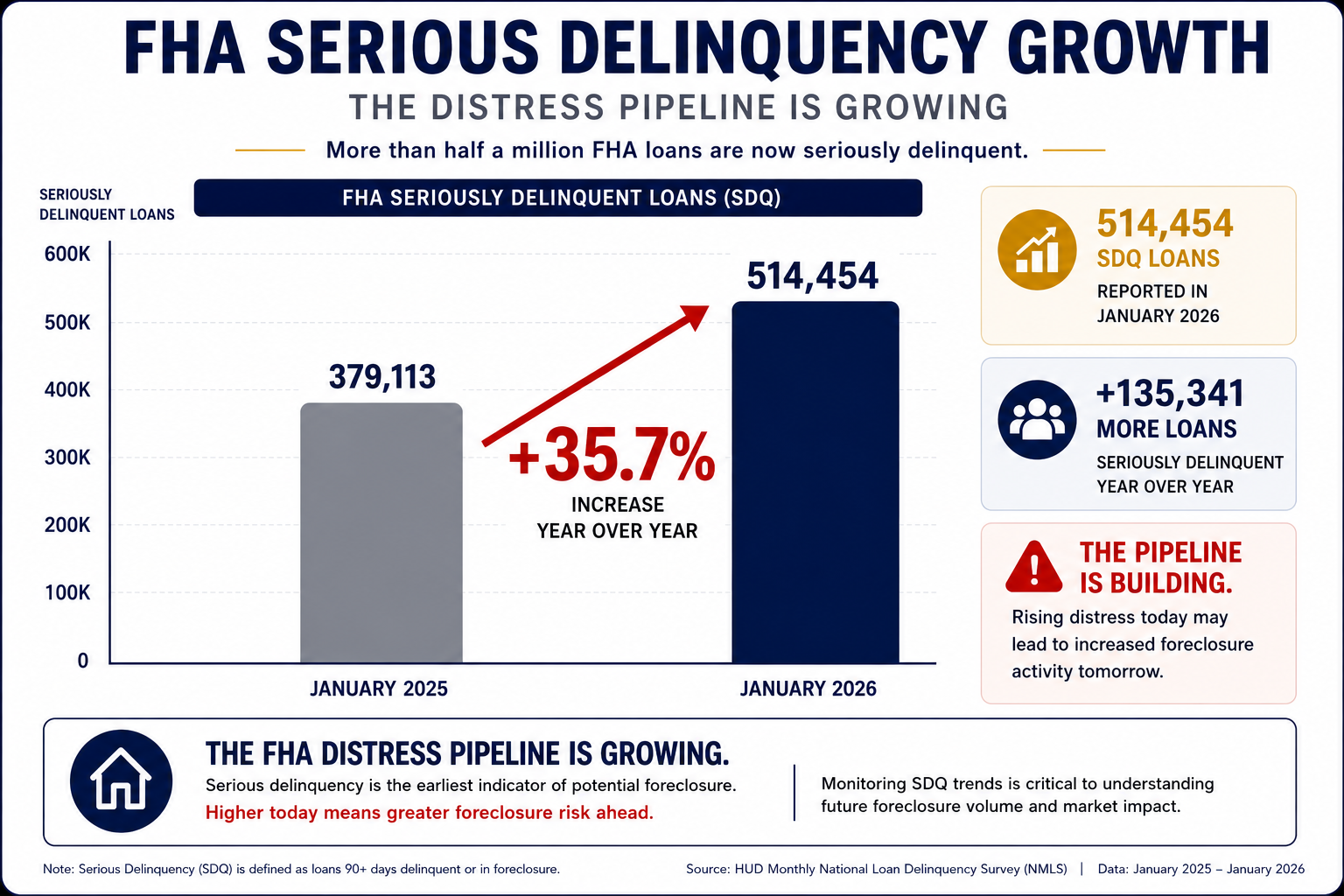

Meanwhile, the distress pipeline itself continues growing.

HUD data showed:

That is more than half a million households already deep in distress.

And if more distressed properties continue resolving upstream through third-party channels, public HUD inventory may increasingly represent only a small visible slice of the larger system behind it.

In other words:

This article is not arguing that investors should disappear from the process.

They serve a role.

Some distressed homes genuinely require capital, speed, and rehabilitation work ordinary buyers cannot absorb.

But the public conversation around FHA foreclosures still sounds like ordinary families are standing at the front door of opportunity.

The numbers suggest many are arriving after the room has already emptied out.

And that may be the real story hiding underneath all of this.

Not that the houses disappeared.

But that the affordable opportunity disappeared before ordinary people ever had a fair chance to reach it.